Late again. This time, I have a better excuse than usual: I wasn’t going to write another report with 💎 Sniper bot still unshipped. It’s now live. The rest you can judge for yourself.

the market

Here’s the strange part about the current market. The macro looks the best it ever has for crypto. Bitcoin ETFs are real, institutionalization is real, banks competing for stablecoin mandates is real, and US legislative momentum is real. The Clarity Act – the first serious US market structure bill in years – cleared the Senate Banking Committee on May 14 with a 15-9 bipartisan vote, and Bitcoin printed a three-month high above $82K on the same set of catalysts (Iran de-escalation, the Clarity vote, broader risk-on). From thirty thousand feet, the chart looks like everything is fine.

Underneath, it isn’t. Coinbase laid off 14% of its workforce on May 5, posting their worst quarterly earnings ever as a public company – Q1 revenue down 26% year over year, trading volumes at their lowest since October 2024. The first version of this app launched mid-2019, and certainly since then, there hasn’t been a market this bad.

What’s different this time is that the macro and the micro have decoupled. Usually, a market this brutal comes paired with bad headlines – FTX, China bans, exchange suits, regulatory crackdowns. This one comes paired with the most constructive headlines crypto has ever had.

The reality is worse than it looks, not the other way around.

Bitcoin’s early-May rally peaked around $82K and has been fading since. Whether Clarity becomes the next narrative that pulls the market out of this – or whether it joins the long list of catalysts that looked sufficient but weren’t – is still ahead of us.

revenue sharing

The revshare program kept growing through the period, but the composition of that growth changed.

- eligible wallets: 210 → 225 (+7%)

- GOOD in revshare: 16.6M → 21.9M (+32%)

- tokens in revshare as % circulating: 10.05% → 10.00%

The wallet count growth slowed from the double-digit pace we’ve had for most of this program’s life. The absolute token count, however, accelerated – the system absorbed ~5.3M new GOOD this period, which is the largest single-month addition since launch. The ratio of eligible GOOD to circulating supply held flat at ~10% as new circulating supply entered through unlocks. So: same proportion of the available pool keeps entering revshare, even as the absolute pool grows.

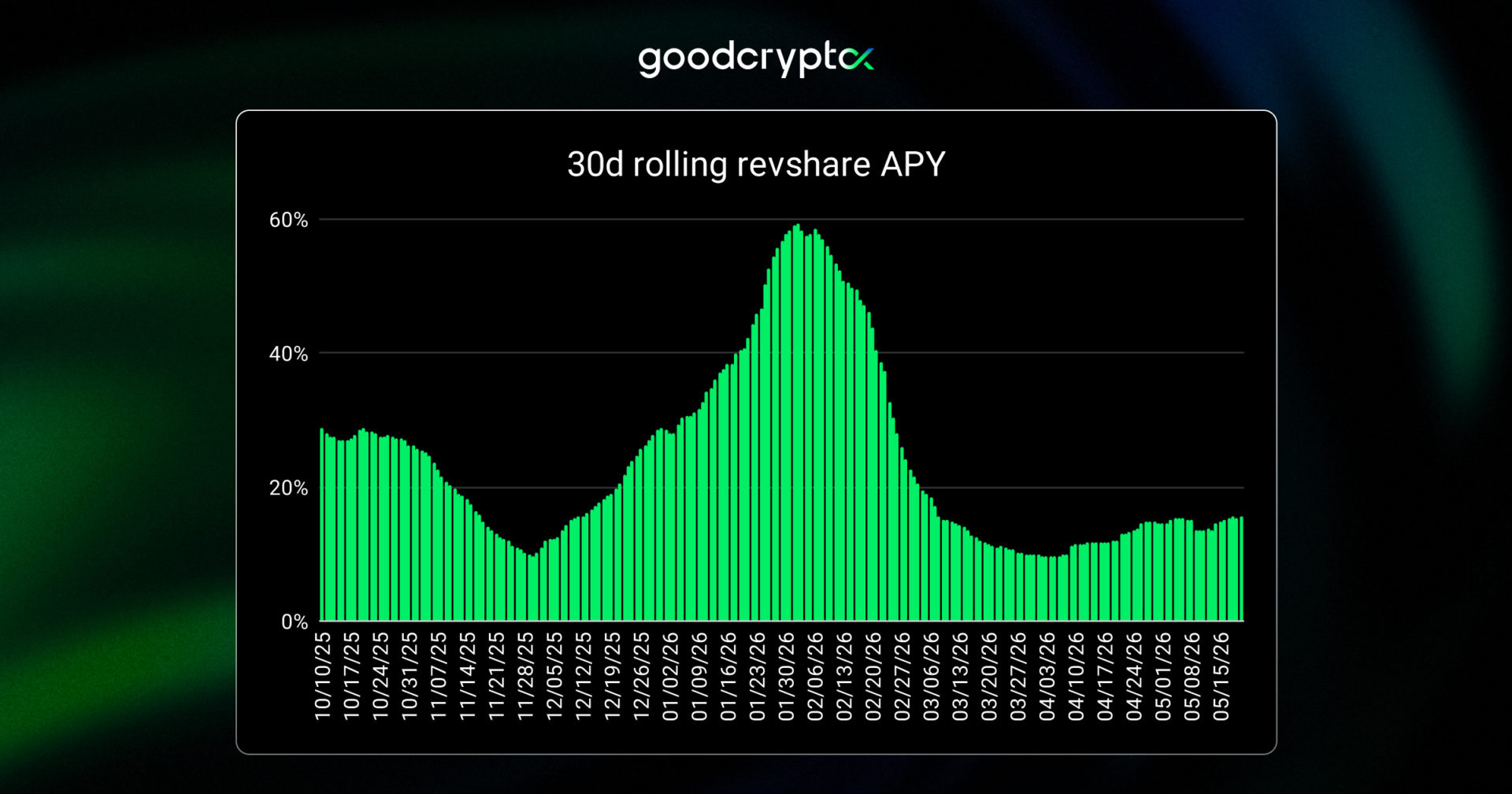

Yields recovered. The 30-day APY climbed from ~11% at the start of the period to 15% by mid-May.

The price of GOOD fell roughly 30% during the period. The eligible token pool grew roughly 30%. These two forces work in opposite directions on APY: more tokens means lower revenue per token, but a lower price means a lower denominator. This month, they roughly canceled each other.

What actually pushed the APY higher despite both is that the underlying revenue grew (a bit) – Hyperliquid volume in particular kept compounding. So the 15% is a real APY, not a price-collapse artifact.

Two other notes from inside the system:

- Auto-compound participation stayed at ~94% of eligible wallets, and the compound mechanic bought back ~274K GOOD from the open market this period. Cumulative compound buybacks to date now sit just above 1.09M GOOD.

- The largest single-wallet share of the eligible pool moved from ~12% to ~22% over the period. One holder consolidated meaningfully.

trading rewards and airdrops

The structural picture hasn’t changed. Trading rewards continue to flow weekly based on in-app volume on both centralized and decentralized exchanges. CEX futures pay $10,000 per GOOD, DEX futures pay $1,000 per GOOD, and GOOD-pair trades earn a bonus (2 GOOD per $100).

Cumulative volume progress toward the announced airdrop thresholds:

- Airdrop 2 → $100M DEX spot volume (now ~$32.4M)

- Airdrop 3 → $1B perp DEX volume (now ~$18.7M)

The DEX spot side moved very little this period – the broader memecoin and Solana retail boom that powered earlier numbers just isn’t there right now. The Hyperliquid side, on the other hand, kept pulling its weight, and then some.

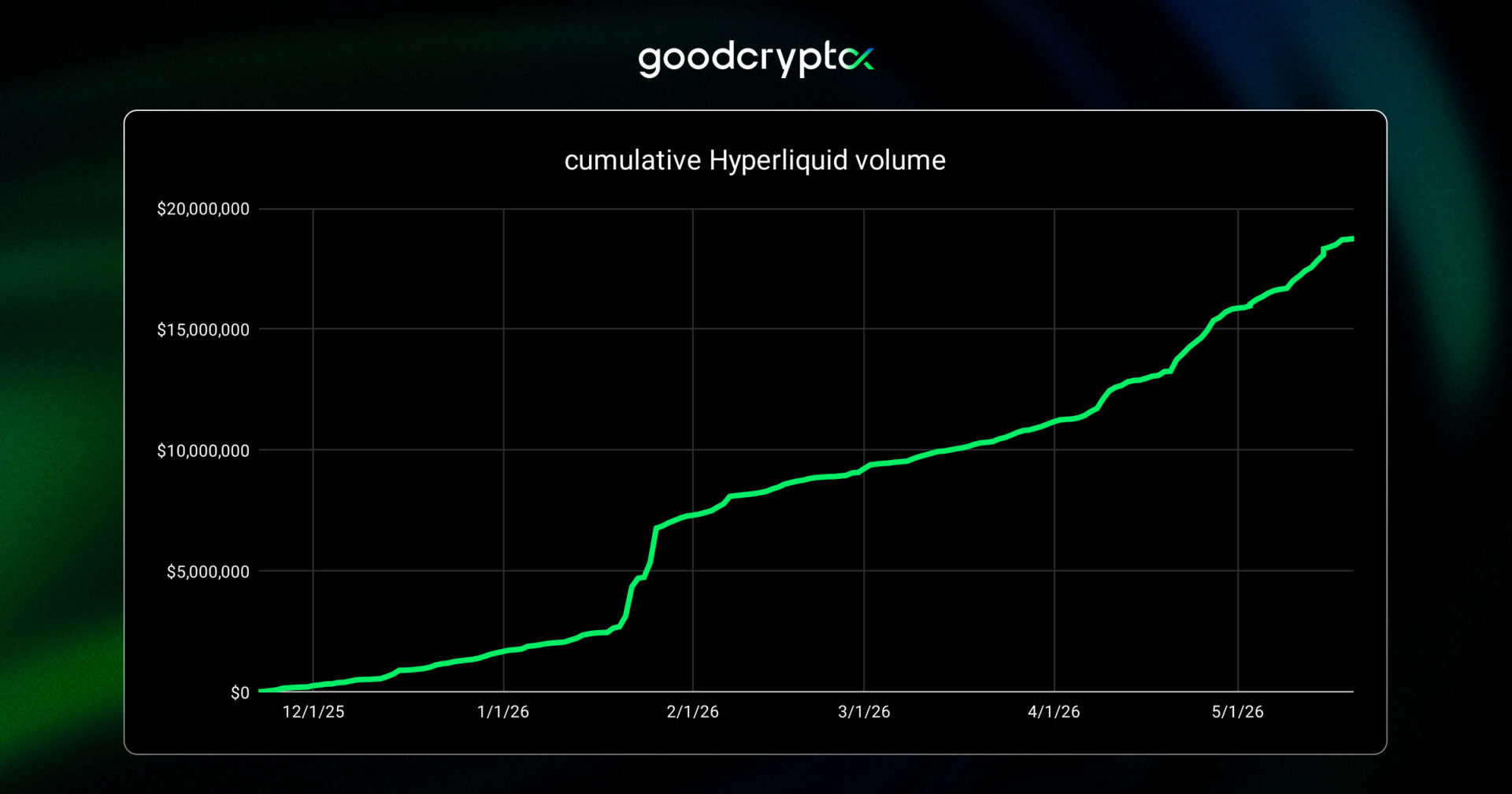

Hyperliquid

Hyperliquid’s contribution to the platform is the story of the period:

- cumulative perp volume: $12.1M → $18.7M

- 30-day daily average: ~$80K/day → ~$166K/day (more than doubled)

- share of total DEX revenue: >50%

Hype volume growth on goodcryptoX is reaccelerating. The monthly volume has gone from $1.5M in M6, to $2.5M in M7, to $4.6M in M8.

burns

The monthly burn came in at ~66K GOOD – down from ~99K last month, reflecting softer CEX & subs revenue.

Daily burns moved in the opposite direction. The period saw ~70K GOOD burned nearly double M7’s. The dynamic that propped daily burns was stronger DEX revenue + weaker price = more tokens burned.

Cumulative burns are now at over 850K GOOD – the 1M 🔥 is getting closer!

the product

💎 Sniper bot (finally) shipped – together with the rebuilt DEX Screener with full Solana support.

The simple version of what 💎 Sniper does: you define filters in the Screener – liquidity, age, launchpad, volume profile, holder distribution – and the bot watches the market for tokens that match. When one appears, it buys, then manages the position with configurable take-profit and stop-loss logic.

The product sounds simple. It isn’t – and that’s why it took time to launch. It is objectively harder to build than it looks, and a lot of that complexity only became fully visible once we launched it with real users at scale.

The release itself was rough. We thought we had tested it thoroughly. We had not. For the first several days after launch, large parts of it didn’t work the way it was supposed to. It’s now stable 🤞 and we’re already seeing users actively exploring the opportunities it brings.

The Screener also got a real upgrade. Full Solana support, broader filter set, and launchpad-based targeting.

Coming next:

- v2.5.1 with quick fixes and native DEX limit orders on Solana

- DEX Grid bot

- continued Sniper improvements – more filters, more execution options, more chains

- the wallet overhaul (Solana + EVM)

- TradingView strategy bots and Screener/Sniper expansion to CEXs

This is not the full roadmap. It’s the near-term track.

zooming out

The framing from last month still holds: The flywheel works. Every time activity shows up, fees, buybacks, burns, and yields all respond. What we’re missing is sustained activity, and that has to come from a new market narrative.

The Clarity Act is the most credible candidate. If it passes, it’s a structural change that can genuinely reshape the market. At some point, the constructive macro translates downward into the activity layer. Or it doesn’t, and we keep building anyway.

Sniper is live. Solana Limit orders are days away. The DEX Grid bot is next. The system is ready. Let’s hope the market recognizes that sooner rather than later.

stay GOOD